If you’re using a VA loan in 2026, your entitlement isn’t just a technical term on your Certificate of Eligibility (VA Loan entitlement 2026). It directly impacts how much home you can afford in Phoenix — especially in Maricopa County – in other words it is your VA entitlement buying power.

Many military buyers assume, “If I qualify for a VA loan, I can buy with zero down.” That’s often true — but not always. Your remaining entitlement, previous home purchases, assumptions, and PCS timing all influence your real buying power.

For a complete breakdown of how VA home loans work for military buyers in Phoenix and near Luke Air Force Base, including eligibility, entitlement, occupancy rules, and repeat use strategy, visit our VA Loan Home Buying Education Hub.

In 2026, VA entitlement affects how much home a military buyer can afford in Phoenix because it determines how much the VA guarantees to the lender. In Maricopa County, eligible buyers with full entitlement can purchase up to the conforming loan limit with no down payment, while buyers with partial entitlement may need to bring money down depending on remaining benefit and local loan limits.

Let’s break this down clearly.

What VA Entitlement Buying Power Really Means

VA entitlement is the amount the Department of Veterans Affairs guarantees on your loan. It is not a loan amount itself — it’s a guarantee to the lender.

There are two types of entitlement:

- Full entitlement – Typically available if you’ve never used your VA loan, or your previous loan has been fully paid off and entitlement restored.

- Remaining (partial) entitlement – Applies if you still own a home with a VA loan, completed an assumption, or experienced a short sale or foreclosure.

If you need a deeper breakdown of how entitlement works, read our full guide on VA loan entitlement 2026.

For this article, we’re focused on how entitlement affects buying power.

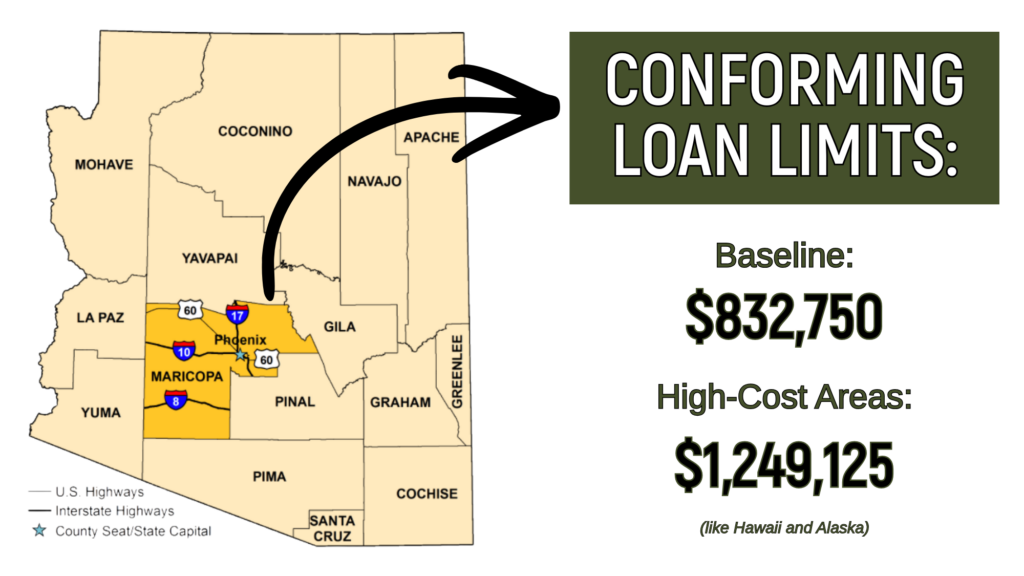

Maricopa County Loan Limits and Buying Power

In 2026, Maricopa County loan limits follow the current conforming standards established by the Federal Housing Finance Agency (FHFA). While VA loans technically have no official loan cap for borrowers with full entitlement, lenders still use conforming limits to determine zero-down eligibility. This directly impacts the answer to your question, “how much can I afford with VA entitlement?” because even if you can afford more, you may have a relevant limit.

Here’s what that means in practical terms:

If you have full entitlement, you can typically purchase above the conforming loan limit with no down payment — as long as you qualify based on income, credit, and debt-to-income ratios.

If you have partial entitlement, your remaining entitlement determines how much the VA will guarantee — and that may require a down payment.

For example:

- A buyer with full entitlement purchasing a $550,000 home in Phoenix may qualify for zero down.

- A buyer with partial entitlement may need to put down 25% of the amount above what their remaining entitlement covers.

- A buyer who completed a VA assumption and did not restore entitlement may have reduced buying power until it is reinstated.

The key point: entitlement affects your down payment requirements — and that directly impacts affordability.

How Partial Entitlement Changes Your Buying Power

Partial entitlement often applies when:

- You kept your previous home and converted it to a rental.

- Someone assumed your VA loan but did not substitute their entitlement.

- You experienced a short sale or foreclosure.

- You bought previously and have not restored entitlement.

In these cases, your available entitlement may not fully cover a new purchase in Phoenix.

That does not mean you cannot buy again. It simply means the structure changes.

For example:

If you still have a VA loan on a property in another state and are PCSing to Luke Air Force Base, you may be able to use remaining entitlement — but your required down payment will depend on:

- Remaining entitlement amount

- Current Maricopa County conforming limits

- New purchase price

- Your lender’s overlays

This is where strategy matters.

Military families often assume they must sell before buying again. That is not always true — but the math must be reviewed carefully.

For a deeper dive on repeat usage, read how to use your VA loan after a PCS.

How PCS Moves Affect Your Entitlement Strategy

PCS moves introduce timing and occupancy considerations.

If you:

- Keep your current home

- Convert it to a rental

- Buy near Luke AFB

- Or receive orders sooner than expected

Your entitlement structure directly impacts whether you can purchase with zero down.

Additionally, VA occupancy rules require that you intend to occupy the property as your primary residence. If your orders change, you’ll need to understand how those rules apply.

We break that down in detail in our guide on VA loan occupancy rules for PCS buyers.

Entitlement, occupancy, and timing all work together.

Real Phoenix Examples (2026 Scenarios)

Here are simplified 2026 scenarios based on common military buyer profiles in the Phoenix metro area:

Scenario 1: First-Time Buyer (Full Entitlement)

An E-6 PCSing to Luke AFB wants to purchase a $500,000 home in Surprise.

With full entitlement and strong income, zero down may be possible.

Scenario 2: Repeat Buyer (Rental Retained)

An O-3 previously bought in Texas using a VA loan and is keeping that home as a rental.

Remaining entitlement must be calculated to determine if zero down is possible in Maricopa County.

Scenario 3: Prior Assumption Without Restoration

A buyer completed a VA loan assumption but did not restore entitlement.

Buying power is reduced until entitlement is reinstated or structured strategically.

Each situation produces a different affordability outcome — even with the same rank and income.

That’s why entitlement cannot be viewed in isolation from your PCS timeline or long-term goals. Here is a full PCS Guide and Checklist to help you get started.

Arizona School Choice & Why It Matters for PCS Families

If you’re relocating to Phoenix or the West Valley, school flexibility may also factor into your buying decision.

Arizona offers both open enrollment and the Empowerment Scholarship Account (ESA) program, giving families significant flexibility in selecting public, charter, private, or alternative education options. This flexibility often reduces pressure to buy in a specific district immediately after a PCS move.

Understanding both your entitlement and your relocation flexibility allows for more strategic decision-making.

When to Schedule a Strategy Call

If you’re PCSing to Luke Air Force Base or buying in the West Valley and want to understand exactly how your VA entitlement impacts your price range in 2026, the smartest next step is to run your numbers before you start touring homes.

Every military buyer’s situation is different.

Remaining entitlement, county limits, BAH, debt-to-income ratios, and long-term plans all shape your buying power.

If you’d like clarity on what you can comfortably afford — and whether zero down is realistic in your situation — schedule a strategy call with our team.

You can also explore available homes near Luke AFB to see what’s currently on the market.

Final Thoughts

VA entitlement is one of the most powerful benefits available to military families. But in 2026, in a market like Phoenix, understanding how it affects buying power requires more than a quick online calculator.

When structured properly, your VA benefit can support not just one purchase — but a long-term wealth strategy across multiple PCS moves.

The key is knowing how your entitlement actually works before you make your next move.

+ show Comments

- Hide Comments

add a comment